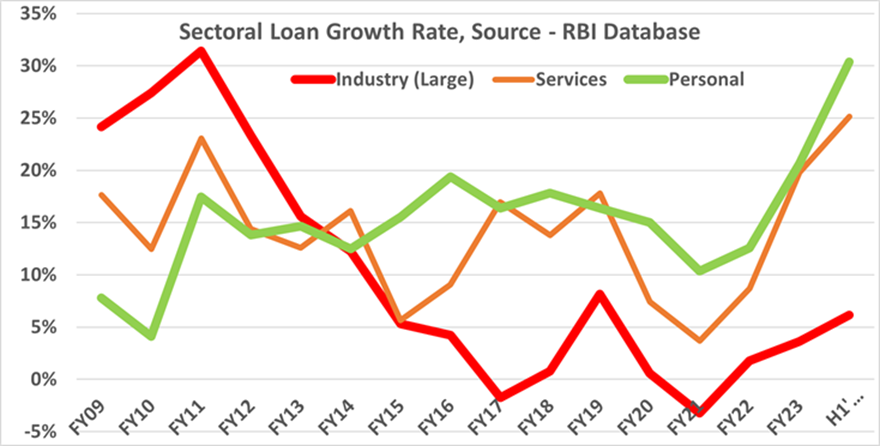

The recent move by RBI to increase the risk weight on certain categories of retail loan and bank loan to NBFCs is a pre-emptive measure to manage the buildup of stress. These segments have recorded significantly higher growth rates over last about 1½ years. So, what is the size of various segments and what is […]